In an era where the digital landscape is rapidly expanding, the financial industry is witnessing a profound transformation in the way it verifies customer identities. Traditional Know Your Customer (KYC) processes, known for their paperwork-intensive and time-consuming nature, are being replaced by innovative Digital KYC solutions. Here in this blog, Neokred will make you dive deep into the intricacies of Digital KYC, exploring its evolution, significance, technologies, implementation challenges, and the future it promises. So let us start and first look at the evolution of KYC.

Evolution of KYC

The evolution of Know Your Customer (KYC) processes has undergone a remarkable transformation over the years. Originating in a time dominated by manual paperwork, KYC involved customers physically submitting documents for identity verification. As the digital age dawned, the limitations of traditional KYC became apparent, prompting a shift toward electronic methods. Regulatory bodies globally tightened KYC requirements in response to heightened concerns about financial crimes and security threats. Digital KYC emerged as a solution, leveraging technology to streamline and enhance the accuracy of identity verification. This evolution is marked by the incorporation of innovative components such as biometric authentication, artificial intelligence, machine learning, and blockchain technology. The transition from paper to pixels not only accelerated the speed and efficiency of the onboarding process but also elevated customer experiences by allowing for secure and convenient digital interactions. In essence, the evolution of KYC reflects a dynamic response to the changing technological landscape, aligning with the imperative for more efficient, scalable, and secure identity verification methods in the digital era.

Understanding Digital KYC

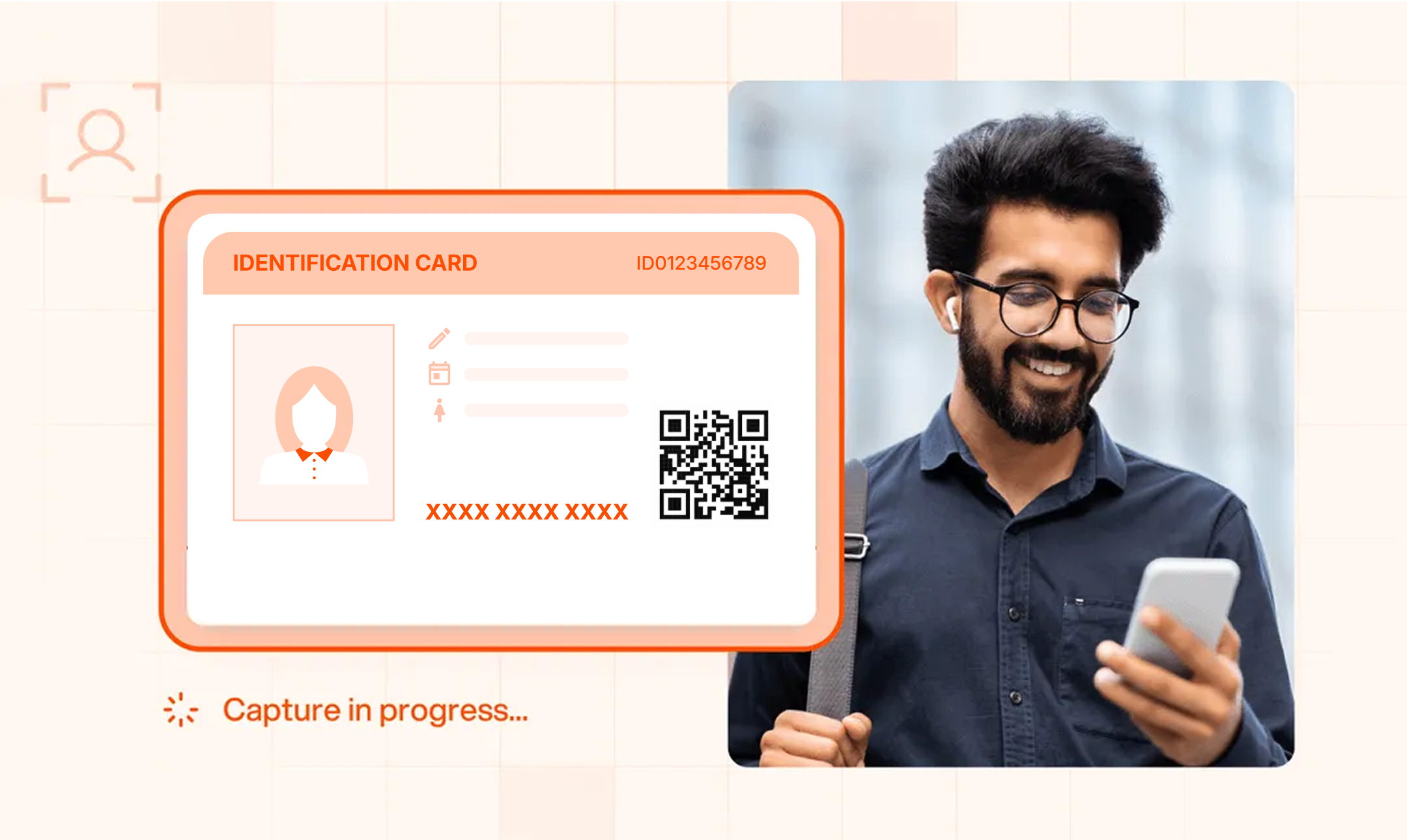

Digital Know Your Customer (KYC) is a revolutionary approach to identity verification that leverages electronic methods instead of traditional, manual processes. In Digital KYC, advanced technologies such as biometric authentication, artificial intelligence, machine learning, and blockchain are employed to streamline and enhance the accuracy of the identification process. This digital transformation allows individuals and entities to verify their identities remotely, eliminating the need for physical paperwork and reducing onboarding times significantly. The multifaceted components of Digital KYC work cohesively to create a seamless, secure, and efficient onboarding experience. Beyond compliance with regulatory standards, Digital KYC contributes to an enhanced customer experience by providing a user-friendly, technologically driven solution to the age-old challenge of identity verification in the rapidly evolving digital landscape.

Now that you have understood KYC and how it evolved, it’s time to understand the technologies powering Digital KYC:

Technologies Powering Digital KYC

1. Biometric Authentication

- Fingerprint Scanning: Utilizing unique fingerprint patterns for precise identification.

- Facial Recognition: Analyzing facial features to confirm an individual's identity.

- Iris Detection: Verifying identity through the distinctive patterns in the iris of the eye.

2. Artificial Intelligence (AI) and Machine Learning (ML)

- Pattern Recognition: AI algorithms analyze vast datasets to recognize patterns and anomalies.

- Predictive Analysis: ML models predict and adapt to evolving identification trends.

- Behavioral Biometrics: Analyzing user behavior for continuous authentication.

3. Blockchain Technology

- Decentralized Storage: Utilizing a distributed ledger for secure, tamper-proof storage of customer data.

- Smart Contracts: Automating and ensuring the execution of predefined KYC processes.

4. Mobile Technology

- Document Capture: Allowing users to securely capture and submit identification documents.

- Mobile Applications: Facilitating user-friendly interactions for KYC processes.

These technologies work in tandem, providing a robust and comprehensive approach to Digital KYC. The amalgamation of biometric, AI, and blockchain technologies, coupled with the convenience of mobile applications, results in a secure and efficient identity verification process in the rapidly advancing digital landscape.

Significance of Digital KYC

The significance of Digital KYC can be understood through its multifaceted advantages that extend beyond traditional KYC methods.

- Efficiency and Speed: Digital KYC revolutionizes onboarding processes by reducing the time it takes for individuals and entities to verify their identities. What once took days with traditional methods can now be accomplished in a matter of minutes.

- Enhanced Customer Experience: The seamless integration of Digital KYC offers customers unparalleled convenience. They can complete KYC requirements remotely, using their preferred digital devices. This user-friendly approach not only simplifies the onboarding process but also elevates the overall customer experience.

- Cost Reduction: Digital KYC leads to substantial cost reductions for businesses. Automation eliminates manual verification processes, decreases paperwork, and mitigates the costs associated with physical document storage. This resource optimization allows businesses to allocate their budget more efficiently and invest in other critical areas of development.

- Compliance and Security: In an era of evolving regulatory standards, Digital KYC ensures businesses remain compliant with global KYC regulations. The integration of advanced technologies, such as biometric authentication and secure data storage, enhances overall security, safeguarding against fraudulent activities and unauthorized transactions.

- Accessibility and Inclusivity: Digital KYC's integration with mobile devices makes identity verification accessible to a wider audience. This inclusivity ensures that individuals from diverse geographical locations can participate in the digital economy, fostering financial inclusion and expanding market reach for businesses.

- Digital Transformation Enabler: Digital KYC aligns with broader digital transformation initiatives within industries. By adopting advanced technologies, businesses not only streamline their KYC processes but also position themselves as innovative leaders in the digital landscape, enhancing their competitive edge.

In essence, the significance of Digital KYC lies in its ability to bring about efficiency, cost-effectiveness, regulatory compliance, and an enhanced user experience. Now at last let us see some of the future landscape of Digital Know Your Customer (KYC):

Future Landscape of Digital KYC

- Technological Innovations: Continuous advancements in biometric authentication, artificial intelligence, and blockchain technology will refine and optimize authenticity enhancement, security, and safety through Digital KYC processes. Innovations such as voice recognition and behavioral biometrics may become integral components.

- Global Standardization: As the demand for seamless, secure, and efficient identity verification grows globally, there is an inclination towards standardization. Industries may converge on common Digital KYC practices, creating a unified approach that transcends borders.

- Expanded Use Cases: Digital KYC will extend beyond traditional financial services, finding applications in sectors like healthcare, e-commerce, and telecommunications. The versatility of Digital KYC will enable businesses to enhance customer experiences across diverse domains.

- Enhanced Ethical Considerations: The ethical dimensions of Digital KYC will garner increased attention. Stricter regulations and industry standards will emerge to address issues like bias in AI algorithms, ensuring responsible data usage, and safeguarding privacy.

- Integration with Emerging Technologies: Integration with emerging technologies, such as 5G networks and the Internet of Things (IoT), will further augment Digital KYC capabilities. Enhanced connectivity and data exchange will contribute to a more robust and interconnected identity verification ecosystem.

A digital KYC solution is a comprehensive and technologically driven approach to identity verification, enabling businesses to efficiently and securely onboard customers while adhering to regulatory compliance. Simplified Digital KYC is a game-changer in finance and digital services. As businesses continue to embrace this digital frontier, the challenges and considerations highlighted here serve as guideposts for navigating the intricate landscape of digital identity verification. The future promises even more advancements, paving the way for a secure, efficient, and customer-centric approach to KYC in the digital age.