Digital KYC is changing how people in India access financial services. You might expect a jump in convenience, but the results are much bigger. In just six years, UPI transactions skyrocketed from 4.5 million to 10 billion per month, all thanks to rapid digital verification. This means the future of banking is not only paperless but also reaching folks who never had access before.

Table of Contents

- Understanding The Digital Kyc Process

- Key Steps In Digital Kyc For Indian Companies

- Benefits For Financial And Payment Services

- Compliance And Security Considerations In India

Quick Summary

| Takeaway | Explanation |

|---|---|

| Digital KYC streamlines onboarding processes | The digital KYC process significantly reduces customer verification time, enhancing efficiency in customer acquisition. |

| Multiple authentication methods enhance accessibility | Various authentication techniques, such as biometric and OTP verification, ensure secure and inclusive access for users across India. |

| Compliance is crucial for digital KYC success | Adhering to the Reserve Bank of India’s stringent guidelines ensures regulatory compliance and protects customer data effectively. |

| Digital KYC fosters financial inclusion | By simplifying verification, digital KYC allows underserved populations to access essential financial services and technology. |

| Robust security infrastructure is mandatory | Organizations must implement advanced security measures to safeguard customer information and prevent unauthorized access. |

Understanding the Digital KYC Process

The digital KYC (Know Your Customer) process represents a transformative approach to customer verification in India’s financial and digital ecosystem. Unlike traditional paper-based methods, digital KYC leverages advanced technological solutions to authenticate and validate customer identities quickly and securely.

The Core Mechanism of Digital KYC

Digital KYC fundamentally reimagines identity verification by utilizing electronic platforms and government-approved identification systems. Learn more about KYC verification techniques that streamline customer onboarding across various sectors. The process primarily relies on Aadhaar-based authentication, which allows individuals to validate their identity through biometric or demographic information.

According to the National Payments Corporation of India (NPCI), the e-KYC Setu System enables regulated entities to verify customer identities without exposing sensitive Aadhaar details. This mechanism significantly reduces operational complexities while maintaining stringent privacy standards.

Authentication Methods in Digital KYC

India has developed multiple digital KYC authentication approaches to accommodate diverse user needs. Research from India Infoline highlights several prominent verification methods:

- Biometric Authentication: Utilizes fingerprint or iris scans for precise identity confirmation

- OTP-Based Verification: Sends one-time passwords to registered mobile numbers

- Video KYC: Enables real-time visual verification through digital platforms

- Offline Aadhaar e-KYC: Allows document-based verification without online connectivity

These methods demonstrate the flexibility and technological sophistication of India’s digital identity verification infrastructure. By providing multiple authentication pathways, digital KYC ensures accessibility while maintaining robust security protocols.

The following table summarizes the major authentication methods used in Digital KYC in India, along with their key features and use cases as described in the article.

| Authentication Method | How It Works | Key Features/Use Cases |

|---|---|---|

| Biometric Authentication | Uses fingerprint or iris scans | High security, precise identity confirmation |

| OTP-Based Verification | Sends one-time password to mobile number | Fast, accessible on basic mobile phones |

| Video KYC | Real-time visual verification on digital platform | Remote onboarding, bridges urban–rural gap |

| Offline Aadhaar e-KYC | Uses Aadhaar XML file for offline verification | No internet required, document-based |

The digital KYC process represents more than a technological upgrade. It signifies a fundamental shift in how financial institutions, government agencies, and service providers interact with customers. Explore how biometrics is transforming KYC and understand the broader implications of this digital transformation.

As Vikaspedia explains, electronic KYC empowers individuals by allowing them to authorize identity information sharing through secure, consent-driven mechanisms. This approach not only simplifies verification but also gives customers greater control over their personal data.

Ultimately, digital KYC is about creating a more transparent, efficient, and user-friendly identification ecosystem that balances technological innovation with stringent security requirements.

Key Steps in Digital KYC for Indian Companies

Digital KYC represents a critical compliance and customer onboarding process for Indian companies across financial, telecommunications, and digital service sectors. Understanding the precise implementation steps ensures regulatory adherence and seamless customer verification.

Comprehensive Digital KYC Application Development

Companies must develop robust digital KYC applications that meet stringent regulatory requirements. Explore our comprehensive e-KYC guide to understand the intricate technical specifications. According to the Reserve Bank of India’s Master Directions, digital KYC applications must incorporate several critical features:

- Secure Access Control: Implement multi-factor authentication mechanisms

- Live Photography Capabilities: Capture real-time customer photographs

- Document Verification Systems: Enable advanced document authentication techniques

Authentication and Verification Protocols

AML India’s research outlines a comprehensive 13-step digital KYC process that Indian companies must rigorously follow. Key verification steps include:

Below is a table organizing the key steps Indian companies must follow for a compliant digital KYC process, as outlined in the article.

| Step | Description |

|---|---|

| 1. Customer Information Collection | Gather essential personal details |

| 2. Identity Document Scanning | Digitally scan IDs (Aadhaar, PAN, etc.) |

| 3. Biometric Authentication | Verify via fingerprint or iris scan |

| 4. OTP Verification | Authenticate with one-time password |

| 5. Final Information Cross-Referencing | Validate all data for accuracy and compliance |

| 6. Digital Document Signing | Complete process using e-signature |

- Customer information collection

- Identity document scanning

- Biometric authentication

- One-time password (OTP) verification

- Final information cross-referencing

The Wikipedia page on eSign highlights an additional critical component: digital document signing through Aadhaar-based authentication. This enables companies to complete verification processes entirely online, eliminating physical document submissions.

Compliance and Data Protection Considerations

Successful digital KYC implementation goes beyond technical steps. Companies must establish comprehensive data protection frameworks that safeguard customer information while maintaining transparent verification processes. This involves:

- Ensuring strict adherence to data privacy regulations

- Implementing encrypted communication channels

- Maintaining detailed audit trails of verification activities

By meticulously following these steps, Indian companies can create efficient, secure, and user-friendly digital KYC processes that meet regulatory standards and customer expectations. The digital transformation of identity verification represents not just a technological upgrade, but a fundamental shift in how businesses interact with and onboard customers.

Benefits for Financial and Payment Services

Digital KYC has revolutionized the financial and payment services landscape in India, offering transformative advantages that extend far beyond traditional verification methods. Learn about seamless financial integration to understand the broader impact of these technological innovations.

Enhanced Customer Onboarding and Accessibility

Financial institutions now experience unprecedented efficiency in customer acquisition and verification processes. According to the Ministry of Finance, digital payments have surged dramatically, with UPI transactions increasing from 4.5 million in January 2017 to an astounding 10 billion in January 2023. This exponential growth directly correlates with the streamlined digital KYC processes that have made financial services more accessible.

The following statistics table highlights UPI transaction growth in India, demonstrating the impact of digital KYC on financial accessibility:

| Year & Month | UPI Transactions per Month |

|---|---|

| January 2017 | 4.5 million |

| January 2023 | 10 billion |

Key benefits include:

- Rapid Verification: Reduce customer onboarding time from days to minutes

- Geographic Flexibility: Enable financial services for remote and underserved populations

- Cost Reduction: Minimize manual processing and documentation expenses

Security and Compliance Advantages

Digital KYC introduces multiple layers of security that traditional verification methods cannot match. Research from financial technology experts highlights several critical security enhancements:

- Biometric authentication reduces identity fraud risks

- Real-time document verification prevents document tampering

- Encrypted data transmission protects sensitive customer information

Regulatory compliance becomes more straightforward with digital KYC. Financial institutions can maintain comprehensive audit trails, ensuring transparent and traceable verification processes that meet stringent government regulations.

Economic and Technological Transformation

Beyond immediate operational benefits, digital KYC represents a fundamental shift in financial service delivery. The technology democratizes access to financial products, enabling smaller institutions and fintech companies to compete more effectively in the market.

The integration of digital KYC with emerging technologies like artificial intelligence and machine learning creates predictive capabilities that help financial institutions:

- Assess customer risk profiles more accurately

- Develop personalized financial products

- Create more inclusive financial ecosystems

As digital infrastructure continues to evolve, digital KYC stands at the forefront of India’s financial technology revolution. It represents more than a technological upgrade it is a strategic approach that balances customer convenience, institutional security, and regulatory compliance.

Ultimately, digital KYC empowers financial and payment services to build trust, enhance user experiences, and drive unprecedented levels of financial inclusion across diverse segments of Indian society.

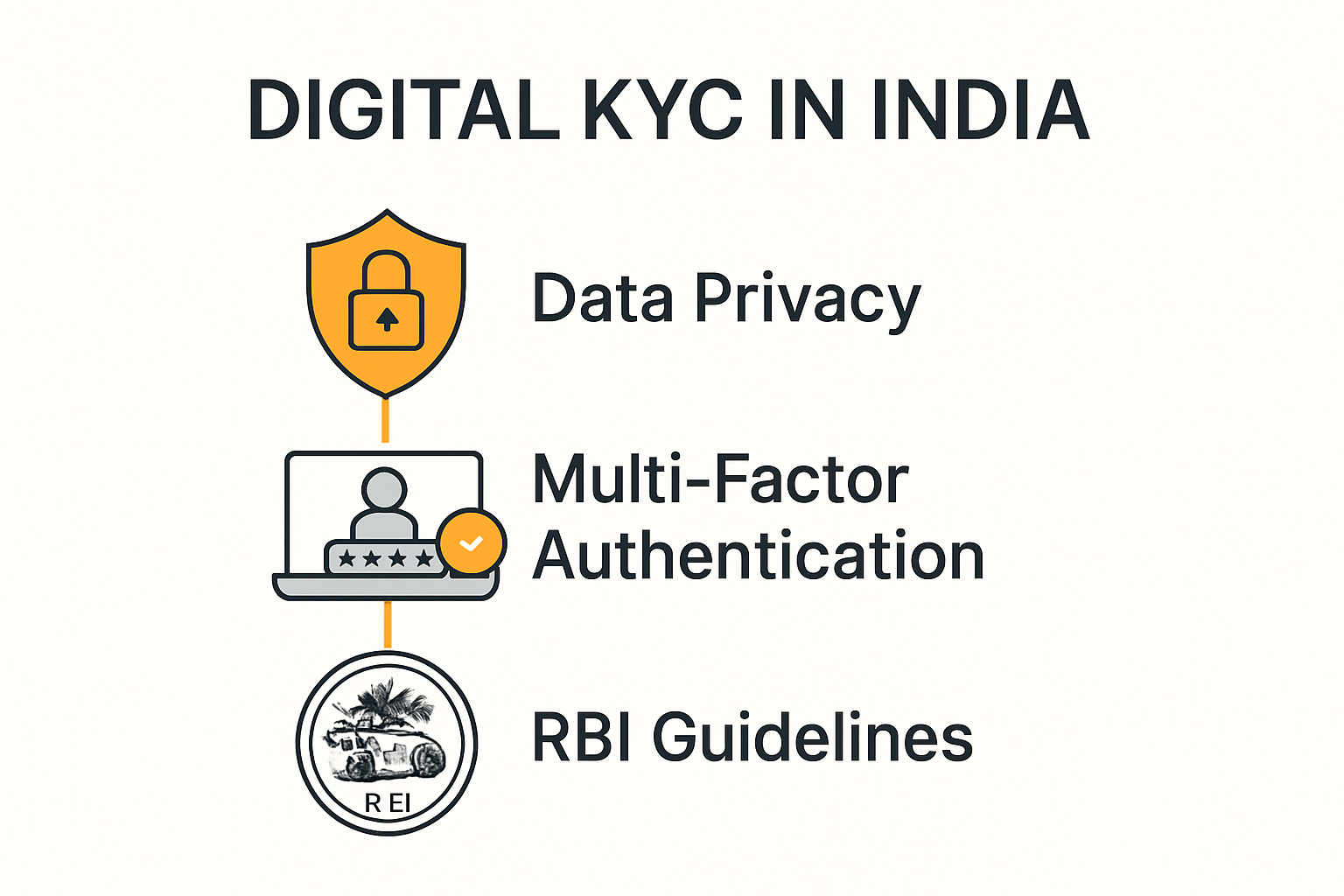

Compliance and Security Considerations in India

Digital KYC in India represents a complex ecosystem of regulatory requirements and technological safeguards designed to protect customer data while enabling seamless digital verification. Understand our comprehensive KYC verification approach to navigate this intricate landscape effectively.

Regulatory Framework and Mandatory Guidelines

The Reserve Bank of India (RBI) has established comprehensive guidelines that form the backbone of digital KYC implementation. According to the RBI’s official notification, regulated entities must adhere to strict protocols that encompass:

- Data Privacy Standards: Implementing robust encryption mechanisms

- Periodic Audit Requirements: Conducting regular security assessments

- Authentication Mechanisms: Using official identity verification channels

The OECD’s 2023 assessment further emphasizes the critical nature of these compliance measures, highlighting the mandatory customer due diligence requirements that organizations must follow.

Technological Security Infrastructure

Effective digital KYC goes beyond mere regulatory compliance. It demands a sophisticated technological infrastructure that can:

- Prevent unauthorized access

- Detect and mitigate potential fraud attempts

- Ensure end-to-end data protection

Key security considerations include:

- Biometric Protection: Advanced encryption of biometric data

- Multi-Factor Authentication: Implementing layered verification processes

- Real-Time Monitoring: Continuous tracking of suspicious activities

Legal and Ethical Considerations

Indian digital KYC regulations strike a delicate balance between technological innovation and individual privacy rights. Organizations must navigate complex legal landscapes that require:

- Explicit user consent for data collection

- Transparent data usage policies

- Comprehensive record-keeping mechanisms

- Immediate reporting of potential security breaches

The regulatory environment demands more than technical compliance. It requires a holistic approach that respects individual privacy while enabling efficient digital verification processes.

Ultimately, compliance and security in digital KYC represent a dynamic ecosystem. Organizations must remain agile, continuously updating their technological and procedural frameworks to address emerging challenges and protect customer interests in an increasingly digital financial landscape.

Frequently Asked Questions

What is the Digital KYC process in India?

The Digital KYC (Know Your Customer) process in India is a technology-driven method of verifying customer identities for financial services. It primarily utilizes electronic platforms, Aadhaar-based authentication, and various verification methods such as biometric scans and OTPs to streamline onboarding and enhance security.

What are the key benefits of implementing Digital KYC for financial services?

Implementing Digital KYC offers several benefits, including faster customer onboarding, improved accessibility for underserved populations, enhanced security through multi-factor authentication, and streamlined compliance with regulatory requirements, ultimately fostering financial inclusion in India.

How does biometric authentication work in Digital KYC?

Biometric authentication in Digital KYC uses unique physical characteristics, such as fingerprints or iris scans, to confirm a person’s identity. This method provides a high level of security and helps to minimize the risk of identity fraud.

What compliance considerations should companies keep in mind when adopting Digital KYC?

When adopting Digital KYC, companies must adhere to guidelines from the Reserve Bank of India, including data privacy standards, periodic audits, and the use of secure authentication mechanisms. Establishing strong data protection frameworks and maintaining user consent are also essential aspects of compliance.

Make Digital KYC Effortless with Neokred

Are you struggling with slow customer onboarding, complex compliance checks, or security gaps in your digital KYC process? This article shows how digital KYC is changing the game in India, but building a seamless, compliant system isn’t easy. Time-consuming manual verifications, privacy risks, and legacy tech often block your growth and make user journeys stressful for both teams and customers.

You deserve a smarter way. Neokred lets you go beyond the basics by providing API-first solutions that automate authentication, enable real-time onboarding, and keep every profile secure and audit-ready. From advanced KYC verification to smooth payment and data privacy integrations, our platform handles the hard work for you. Why wait and fall behind? Visit Neokred now and find out how you can build frictionless digital experiences that meet every compliance need. Start today and become part of India’s digital transformation.

Recommended

Conclusion

Discover how the digital KYC process streamlines verification for financial and payment services in India, boosting compliance and customer experience.